Yahoo is in trouble. We have been assessing it and decided to compile a "snapshot" of all the ongoing onslaught Yahoo has been under with this latest salvo coming out from one of the hedge funds which we are noting here for reference--What we must note is that a franchise that gets around 200 Million Unique Visitors can be quite a coup for anyone:

http://www.businessinsider.

200 Million Vistors

core biz between 2 4 bil

market cap tied to alibaba and yahoo japan at 32 bil

aol helping third party make ads

January 6, 2016

Board of Directors of Yahoo! Inc.

701 First Avenue

Sunnyvale, California 94089

701 First Avenue

Sunnyvale, California 94089

cc: Maynard J. Webb, Chairman

Marissa Mayer, Chief Executive Officer

Larry Sonsini, Esq., Legal Counsel

Marissa Mayer, Chief Executive Officer

Larry Sonsini, Esq., Legal Counsel

Dear Board Members,

The past year has been an extremely frustrating one for shareholders of Yahoo! Inc. ("Yahoo" or the "Company"). We are sure that you, the Board of Directors (the "Board"), must also be frustrated. Despite reasonable intentions, in the end, the proposed spin-off of Yahoo's stake in Alibaba Group Holding Limited ("Alibaba") into Aabaco Holdings, Inc. ("Aabaco") turned out to be a failed effort due to a changing tax landscape and serious concerns over the potential for massive tax liability. We believe you ultimately made the right decision by suspending the spin-off of Aabaco. Also frustrating for us, and likely for you, has been the continued downward spiral of the operating and financial performance of Yahoo's core Search and Display advertising businesses (the "Core Business"). Despite over three years of effort and billions spent on acquisitions, the management team that was hired to turn around the Core Business has failed to produce acceptable results, in turn, causing massive declines in profitability and cash flow.

It appears that investors have lost all confidence in management and the Board. As of Tuesday's close, the value of the "Yahoo Stub" (defined as Yahoo's market value less the value of its shares in Alibaba) has collapsed and is currently trading near zero. The bulk of Yahoo's current market value almost entirely derives from an extraordinary investment Yahoo made over ten years ago in Alibaba, and the good fortune that Alibaba's management team has executed well such that this investment today is worth over $30 billion. This compares to Yahoo's current market capitalization of approximately $30.5 billion.

The current valuation of Yahoo implies either a massive tax liability on Yahoo's minority equity interests in Alibaba and Yahoo Japan Corporation ("Yahoo Japan") or that the remaining operating assets of Yahoo are worthless, or some combination of the two. While we agree that the failed separation has been frustrating, we are confident that a separation of these assets can be accomplished through either a sale of the Core Business or a spin of the Core Business. Either of these outcomes would result in a much more tax efficient separation than the market currently implies. Unfortunately, it appears that shareholders have no confidence that management and the Board will be able to execute on a separation of these assets or improve the performance of the Core Business. We are confident that both of these objectives are achievable, but will require a change in leadership and strategy.

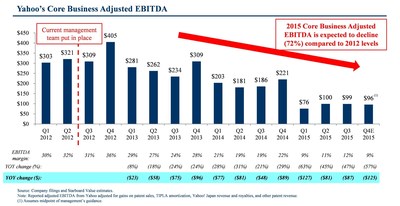

Yahoo's current management has had over three years to demonstrate progress towards improving the Core Business, but despite these efforts, the Core Business continues to be plagued with deteriorating financial performance and an accelerating number of executive leadership departures. Annual operating costs have ballooned, increasing by approximately $500 million despite revenue that has been declining. In addition, the Company has spent over $2.3 billion on acquisitions. Unfortunately, most of these investments have been misguided, poorly overseen, and, ultimately, shut down. Even with these massive investments, the trajectory is decidedly negative. As shown in the table below, EBITDA continues to decline quarter-after-quarter while spending continues at an alarming pace.

If nothing else, the results of the past three years, which follow several other failed attempts to turnaround the business theretofore, should demonstrate to you that turning around this business is extremely difficult. To be successful, dramatically different thinking is required, together with significant changes across all aspects of the business starting at the board level, and including executive leadership. New leadership will have to develop and implement a plan to balance priorities between growth and profitability. This will mean prioritizing and investing in certain parts of the business while at the same time deeply reducing unnecessary costs, selling or exiting many unprofitable businesses and research projects, and overhauling the incentives and compensation programs to instill sound business behavior.

Over the past 13 years, we have been involved in similar turnaround efforts with many of our portfolio companies. Certainly on paper, there could be a viable plan to significantly restructure Yahoo, shift direction under new leadership and attempt, once again, to reverse the current trends of declining revenues, increasing costs, and plummeting profits. We, and you, understand that businesses are not operated on paper and that leadership skill and experience is required for complex turnarounds as well as day-to-day management. We understand that executing such a significant restructuring at an extremely high profile public company while reporting quarterly results is challenging. That is why it is necessary for the Board to remain open-minded regarding the future of Yahoo. The Board must be able to assess and compare a stand-alone spin-off and restructuring of the Core Business, as described above, versus the value that could be received today through a competitive sale process resulting in a sale of the Core Business to a strategic or financial buyer.

We are highly confident that there are interested and credible buyers for Yahoo's Core Business. It is our understanding that even after Yahoo announced its plan to spin-off, instead of sell, the Core Business, several interested parties subsequently reached out to Yahoo's management and Board expressing interest in buying the Core Business. Yet, unfortunately, according to several credible media reports, Yahoo has thus far ignored this inbound interest. This is highly concerning to us because when recently asked specifically on CNBC, Maynard Webb, Yahoo's Chairman, stated that if Yahoo received inbound interest from potential strategic or financial buyers the Board would engage with those parties:

"The Board has fiduciary obligation to engage with any legitimate person that comes forward with a good offer. The Board will always do its fiduciary obligations when something like that occurs." - Maynard Webb, December 9, 2015

This is unacceptable. By making the above statement, while simultaneously ignoring serious interest, you are sending potentially destructive mixed messages. In order to ensure the best possible outcome for shareholders, it is imperative that you clearly communicate your receptiveness to discussions with parties who demonstrate an interest in an acquisition of the Core Business. Those parties can then confidently commit the time needed to make a bid. Only in this way can you truly compare the potential value received in a sale of the Core Business versus a substantial stand-alone restructuring of the Core Business.

For over a year, we have attempted to work constructively with management and the Board of Yahoo. We have tried extremely hard to work "behind the scenes." We have grown increasingly frustrated. It took significant effort for us to convince you it was the right choice to suspend the Aabaco spin-off. Unfortunately, instead of heeding our advice and concurrently announcing that you would explore a sale of the Core Business, you have now hid behind a plan to spin-off the Core Business and Yahoo Japan without fully understanding the alternative options. We have had numerous conversations with you for over a year where we expressed our extreme concern with the trajectory of the Core Business. We told you that, aside from separating the minority equity interests, the performance and lack of turnaround execution on the Core Business was our primary concern and focus. You assured us for over a year that you had a plan for execution and that you were confident that 2014 would be a low point for EBITDA. We explained over and over again that we did not believe your actions, or lack thereof, would achieve the desired result of stabilizing the business. Unfortunately, it appears we have been right, and each quarter is worse than the last. Your solution to just announce a change in direction of the spin and that it will require another year for shareholders to wait while the existing leadership continues to destroy value is not acceptable.

The Board must accept that significant changes are desperately needed. This would include changes in management, changes in Board composition, and changes in strategy and execution. If the Board is willing to embrace the need for significant change and pursue a strategy along the lines of what we have proposed above, we are hopeful we can work constructively together and make changes to the Board through a mutually agreeable resolution. This is clearly the preferable route. If the Board is unwilling to accept the need for significant change, then an election contest may very well be needed so that shareholders can replace a majority of the Board with directors who will represent their best interests and approach the situation with an open mind and a fresh perspective. The new Board can then assess the state of the existing business, including a review of management's strengths and weaknesses, so that the Board can best represent shareholders in analyzing a viable turnaround plan compared with potential offers for the Core Business. We look forward to our continued discussions.

Respectfully,

Jeffrey C. Smith

Managing Member

Starboard Value LP

Managing Member

Starboard Value LP

About Starboard Value LPStarboard Value LP is a New York-based investment adviser with a focused and fundamental approach to investing in publicly traded U.S. companies. Starboard invests in deeply undervalued companies and actively engages with management teams and boards of directors to identify and execute on opportunities to unlock value for the benefit of all shareholders.

Investor contacts: Peter Feld, (212) 201-4878

Gavin Molinelli, (212) 201-4828

www.starboardvalue.com

Gavin Molinelli, (212) 201-4828

www.starboardvalue.com

This was a 100-slide presentation done last month:

http://www.businessinsider.

| |||

|

| WEDNESDAY, DECEMBER 9, 2015 | |||||||

TOP STORY

Deal Professor: Marissa Mayer Has a Year to Fulfill Yahoo's Potential With Yahoo's one billion users and revenue of nearly $5 billion, investors would be salivating if Yahoo were a start-up, not a faded Internet company.

| |||||||

| |||||||

QUOTATION OF THE DAY"If someone came in today and made offers on what the core or operating business is worth today, it would probably be a lowball offer."- Maynard Webb, the chairman of Yahoo. |

| |||||

core biz between 2 4 bil

market cap tied to alibaba and yahoo japan at 32 bil

aol helping third party make ads

The Fortune's Geoff Colvin once again noted this in his usual direct matter of fact dilemma that ultimately resulted in the letter released today:

|

|

|

| FOLLOW | SUBSCRIBE | ANON TIP |

| November 20, 2015 |

| Marissa Mayer’s three-year effort to turn around Yahoo has been a major-league leadership saga, as it was destined to be. Events of the past few days suggest – but don’t yet dictate – that the saga is in its final chapters. Yahoo was a mess when Mayer left Google to take over as CEO in July 2012. At that time no major troubled Internet company had ever been turned around, and this looked like as good a test as any of whether it was even possible. Mayer had been a star executive at Google and was widely hailed as a brilliant hire. In a sense she has done what she was hired to do, changing strategic direction and making bold investments. But the numbers tell the unhappy story of how her moves have worked out so far. Yahoo’s market cap is $31 billion. Its stake in Alibaba (acquired long before Mayer arrived) is worth $30 billion, and its stake in Yahoo Japan (ditto) is worth $8.1 billion. Apply some tax-related discounts to those values to reflect what the company could actually net by selling, and add $7.6 billion of cash and other current assets Yahoo held as of September 30, and we see that investors figure Yahoo’s actual businesses are worth approximately nothing. That situation is not, as they say, sustainable. Fortune’s Erin Griffith explains how activist investor Jeffrey Smith’s Starboard Value Fund bought a big stake in Yahoo last year and reasonably urged Mayer to off-load its Alibaba and Yahoo Japan holdings so investors could buy or sell them separately from Yahoo. Mayer developed a plan to do so but ran into a problem: The IRS would not assure Yahoo that spinning off those investments in the way planned would be tax-free. Yahoo’s board decided the risk was worth taking and announced it would go ahead. Now Smith has concluded the plan is too risky and is pressing Mayer and the board to do the opposite, sort of – sell Yahoo’s core operating businesses wholly or in pieces for whatever they might fetch, leaving Yahoo as merely a vessel for owning shares of Alibaba and Yahoo Japan. Smith argues that without such drastic action, Yahoo is in an irretrievable vortex of doom because it can’t attract top-level talent with stock incentives, since the stock’s performance merely reflects the performance of Alibaba and Yahoo Japan. Without the best talent, the company can never build its business to a point where it outweighs the performance of the Asian assets, leaving the company forever trapped. Of course Mayer disagrees vehemently with that reasoning, telling Wall Street analysts recently that the company is well positioned “to deliver long-term sustainable growth for our investors.” But investors have zero reason to believe her assurances, which is why envisioning any kind of long-term future for Yahoo is growing increasingly hard. Maybe no one could have saved Yahoo. Or maybe Mayer still can and will. But how about this for a leadership challenge: One way or another it seems likely that Yahoo’s businesses will soon be standing on their own, trying to persuade the world that they’re worth anything at all. |

No comments:

Post a Comment